INDIANA – Today, the Indiana Institute for Working Families released a new policy brief: Debt in Indiana.

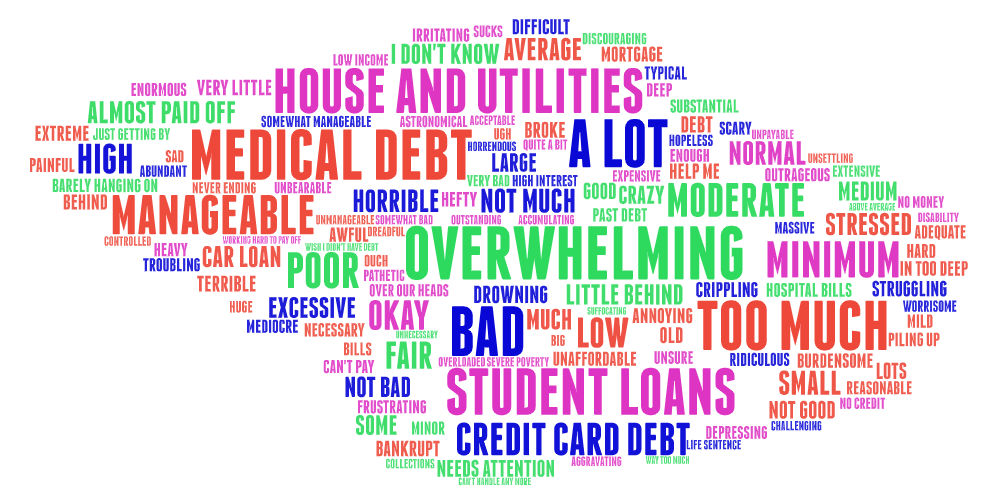

While debt can be an effective tool for consumers to achieve a financial goal, a patchwork of protections – at both the federal and state levels – can lead consumers towards a spiral. It should be unsurprising then that when asked to describe the debt they currently have, clients from Indiana’s Community Action Agencies responded with words like “overwhelming,” “horrible,” and “excessive.”

The policy brief

- Summarizes debt characteristics from a large survey conducted by the Indiana Community Action Association (INCAA);

- Provides trends in debt, delinquencies, and debt collections in Indiana; and

- Recommends policy changes that would address issues that exacerbate or create pressures of owning debt.

Indiana Community Action Association Survey Results: Debt Characteristics

During the fall of 2020 and the spring of 2021, INCAA, through its 22 local agencies covering all 92 counties, issued a survey to neighbors and clients to collect demographic, general well-being, COVID-19, and data on other key areas of interest. Survey respondents (5,882 total) were asked to identify both the type of debt (among six choices) and amounts (within specific ranges). Those surveyed were also asked if any of the six debt types were in collections. Descriptive statistics for debt-related questions are discussed below.

Types of Debt & Balances

Medical debt was the most common type of debt reported, with nearly half (47 percent) of all respondents indicating they had medical debt outstanding. While student loans were not as prevalent among respondents compared to other types of debt, student loan balances tended to be higher as 64 percent of respondents had student loan balances of more than $10,000. Median gross monthly incomes among respondents with debt varied slightly, ranging from $1,480 for those with medical debt to $1,790 for those with auto loans. However, median monthly incomes of those with debt were above the median across the entire survey ($1,290 per month)

Disparities by race and gender were present among survey respondents. In particular, Black respondents were over twice as likely to have a payday loan as their White counterparts. Among those with student loans, Black respondents were 83 percent more likely to have student loans than White respondents. Black respondents with student loans tended to have higher balances as well with 69 percent of black student loan borrowers having balances over $10,000 compared to 62 percent of white borrowers. By gender, the disparity among student loan borrowers was also present as women were more than twice as likely to have any student loan debt as men. Similar to the disparity between Black and White respondents, the gender disparity was most acute among borrowers with more than $10,000 in student loan debt – 64 percent of female student loan borrowers compared to 55 percent of males.

Debt in Collections

Survey results indicated that half of all respondents had at least one debt in collections and nearly a quarter (23 percent) had two or more debts in collections. Medical and credit card debts were the most common types in collections and the most prevalent among respondents.

Black respondents were more likely to have each type of debt in collections than white respondents. In fact, black

respondents were nearly three times more likely to have a payday loan in collections than their white counterparts and over twice as likely to have student and car loans in collections, respectively. Similar disparities were observed by gender as women were nearly twice as likely as men to have student loans in collections.

Indiana Trends: Household Debt & Collections

In the year defined by a global pandemic, total household debt in the United States and in Indiana reached new heights.

According to the Federal Reserve Bank of New York, nationwide household debt increased by $414 billion (3%) from

2019 to 2020, and initial data for 2021 show this trend may continue through the year.vi Statewide debt levels in Indiana increased at a slightly higher rate (3.6 percent), increasing by roughly $8 billion to $226.5 billion in 2020. This total level equates to $40,770 in household debt per Hoosier (per capita).

Non-mortgage household debt per Hoosier, including auto loans, credit cards, and student loans, has been steadily

increasing since the earlier 2000s and through the 2008-2009 Great Recession. Most notably, student loans as a share of all household debt per capita have more than doubled over the past 15 years. This is unsurprising given the increased availability of federal and private student loans combined with the rising costs of higher education.

Delinquencies & Collections

Pressures stemming from slow-to-nonexistent wage growth, particularly among low-income, non-White, and female workers, respectively, leave little surprise that many households struggle to cover a $400 expense or to stay current on debt payments. As borrowers fall further behind and delinquent on payments (after 90 days), they face the added risk of the debt being recouped through the collection process

Indiana delinquency rates for household debts have remained relatively stable over the past five years, Due in

part to the federal response to the COVID-19 pandemic, delinquency rates have even fallen – especially student loans in 2020 – as automatic or optional forbearance options, stimulus payments, and enhanced unemployment insurance

benefits provided much-needed security to the most vulnerable workers and families.

The recent drop in student loan delinquency rates can likely be attributed to the federal response to COVID-19. Delinquencies and collections hit low-to-moderate-income Hoosiers at disproportionate rates. While low-to-moderate income consumers tend to have less debt or no debt at all, these consumers are over twice as likely as middle-to-high

income consumers to have a debt severely delinquent or in collections.

Similar discrepancies are evident between white communities and communities of color, contributing to the persistent and growing racial wealth gap.

Policy Recommendations

Establish a maximum, all-in allowable APR at 36 percent and avoid policies that allow lending products to significantly increase the effective costs to consumers. A maximum rate including all fees and finance charges would be a demonstrable step in limiting and preventing predatory lending practices both in Indiana and nationwide. Currently, Indiana is just one of 25 states without strong rate caps. This lack of protection supports debt traps at APRs as high as 391 percent on payday loans. A 36 percent APR has been long recognized and supported by federal regulators and the Department of Defense as a way to combat predatory lending practices and usury while maintaining profitability for lenders. Bipartisan legislation at the federal and state level has been historically introduced to address this issue

Enhance financial assistance policies to ensure medical treatment is more affordable for low-income patients. Indiana is one of a handful of states that does not require all hospitals (nonprofit and private) to provide financial assistance policies nor does the state mandate the eligibility standards for patients who need assistance. Generally, very low-income patients (below 75% of the Federal Poverty Level) are eligible for financial assistance for very severe medical conditions at nonprofit Indiana hospitals.xxv Policy specifics are adopted at the county or hospital level

Prevent medical debts from being reported to credit bureaus until billing is finalized. Currently, medical debts in the dispute or under review can be placed as delinquent or in collections on a consumer’s credit report. Federal legislation to provide a one-year or longer waiting period would provide consumers with the opportunity to resolve any outstanding claims while protecting their credit scores and reports.x

Reform process for student loans to be discharged through bankruptcy. Allowing all student loans to be discharged in bankruptcy would provide meaningful relief for borrowers who cannot pay while ensuring parity between student loans and other debts within the bankruptcy process. While it is possible for borrowers to have student loans discharged in bankruptcy, borrowers must prove that repayment would cause an undue hardship, which poses difficulties

Streamline income-based repayment plans for federal student loans into a single repayment plan. The current patchwork of different income-driven repayments causes unnecessary complexity for federal borrowers and jeopardizes a true ability to repay student loans. A new, streamlined repayment program that caps repayment at a certain percentage of discretionary income would provide a pathway for borrowers to repay their loans while also ensuring borrowers can meet their basic needs.

Reduce harassment in collections and ensure basic needs are preserved when wages are garnished. In 2020, the

Consumer Financial Protection Bureau (CFPB) issued a two-part rule aimed at debt collection practices that would affect 68 million Americans. There is a small window of time left to strengthen the rule on behalf of consumers before it goes into effect on January 29, 2022. Additionally, current wage garnishment thresholds only protect a small portion of wages ($217.70 per week). xxx This threshold should be raised to protect a consumer’s ability to meet their basic needs and to prepare for a financial emergency.

Protections should be extended that prohibit student loan borrowers from having their tax refunds, social security payments, and other federal payments garnished as permitted by current law. Promote financial literacy and education. In an economy that maintains strong consumer protections, provides a livable wage, and promotes equity and fairness, financial literacy and education can reach their full potential. Services provided by community-based organizations such as Centers for Working Families and Community Action Agencies can help consumers and families obtain the necessary skills to reach financial stability. Unfortunately, current imbalances and disparities present an uphill battle that financial literacy cannot remedy on its own.